Floridians Don’t Have to Wait as Long to File Bad Faith Suits

Dealing with insurance claims involves a lot of waiting. Even though we have email and instant messaging, policyholders still find themselves waiting for snail mail and other slower forms of communication for processing.

This isn’t just frustrating; it means that medical bills from the treatment of your injuries and other expenses continue to pile up, and negatively impact your life.

The longer you have to wait for compensation, the more interest accrues if you were forced to use credit, and the longer it takes for you to resume your normal life.

Florida legislators see this issue, and they are now helping the insured hold insurance companies accountable faster.

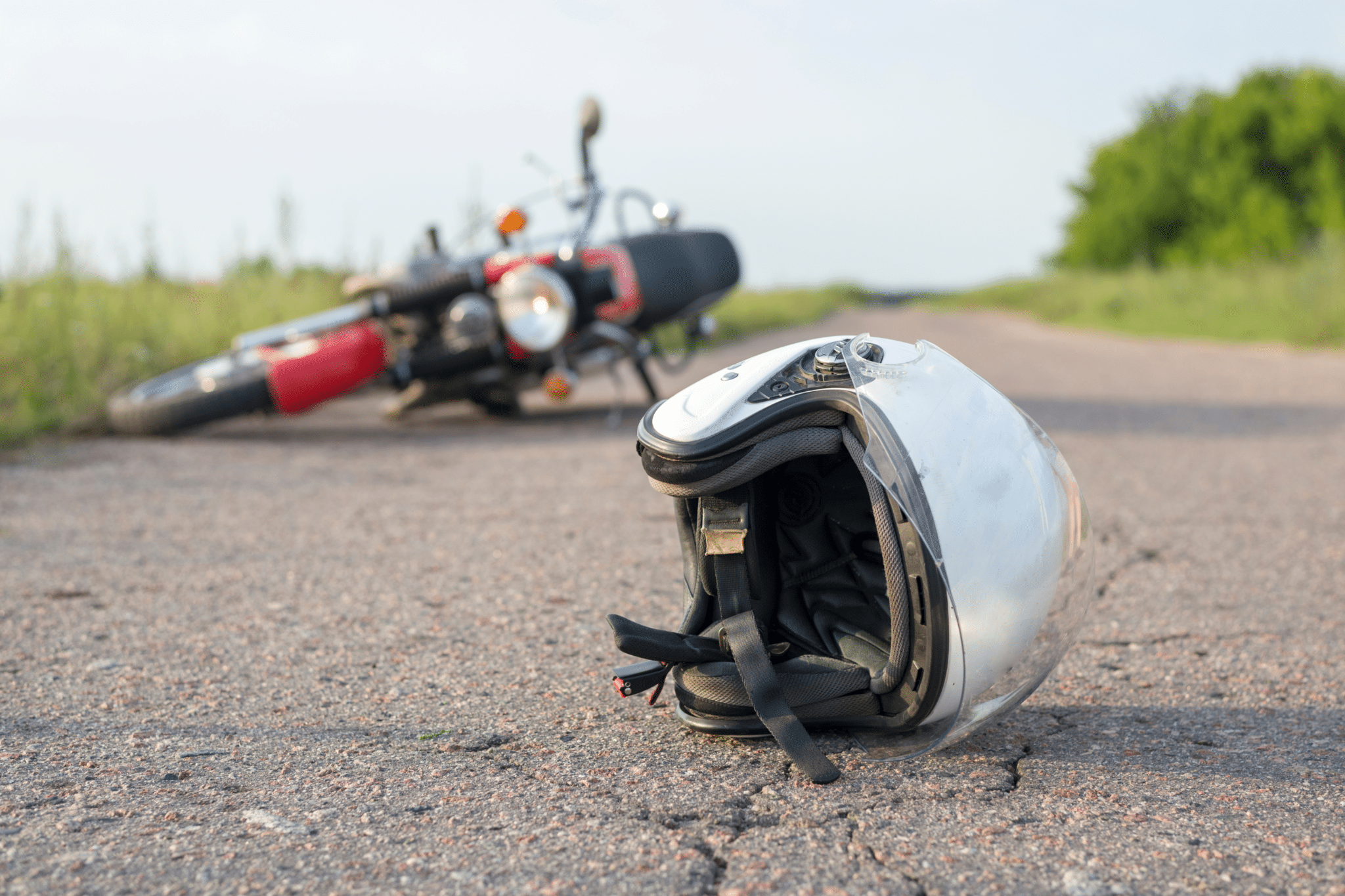

A recent case (Harper v Geico) in the Florida Appellate Court examined these wait times. As a result, their decision will potentially speed up the process of filing a bad faith claim, allowing you to receive the compensation you’re due faster, too.

Harper v GEICO Case Background

While Harper v GEICO was decided in early March 2019, the story of this case actually begins in 2013. Serenity Harper was involved in a serious auto accident, and after the accident, she filed for coverage twice.

Both Harper and the at-fault driver had insurance through GEICO. She filed under the at-fault driver’s liability coverage and under her underinsured motorist (UM) coverage.

GEICO paid the first claim but refused multiple times to pay the UM coverage.

The “Cure Period” for Civil Remedy Filings

Harper electronically filed a civil remedy notice (CRN) on December 18, 2013. She sent a file of the notice through the mail to GEICO shortly after, and GEICO received the physical CRN on December 26, 2013.

Here’s where things get confusing. Florida law allows insurance companies up to 60 days after filing the notice for processing. Only once this 60-day “cure period” is over, the insurance holder is legally entitled to file a bad faith claim.

Harper Finds Justice Against GEICO on Appeal

GEICO did pay Harper up to her UM limits, but the official check and release were not sent until February 21, 2014.

Harper’s lawyers argued that the 60-day cure period began once the CRN was electronically filed on December 18 and that GEICO paid only after the cure period was over.

GEICO countered that they did not receive the physical CRN until December 23, and argued that they had met their payment deadline and that Harper was not entitled to file a bad faith claim.

A trial court in Florida sided with GEICO and prevented Harper from filing a bad faith claim. However, once Harper appealed, she won.

The Florida Appellate Court decided that the cure period begins once the insured party files the CRN, rather than when the insurance company receives it.

About Bad Faith Claims in Florida

There are many reasons to file a bad faith claim in Florida. Unfortunately, insurance companies sometimes try to get away with not paying claims or not paying on time.

Insurance companies may have legitimate reasons to deny a claim: your coverage doesn’t cover certain injuries, you filed the paperwork too late, etc. But when you follow correct procedures for filing, there should be no reason that your insurance company strings you along or denies your coverage altogether.

If any of the following occurs, your insurance company might be acting in bad faith:

- The insurance company failed to recognize your claim after you filed it

- The insurance company failed to investigate the claim in a prompt manner

- Communications were received, but not responded to in a prompt manner

- The insurance company attempts to slow down the progression with unnecessary or irrelevant paperwork

- You are never given legitimate reasons for denial of your claim or delays in the process

- You receive less compensation than you should and are not given a reason why

- Your policy is canceled for no legitimate reason

Now, according to the Florida Appellate Court, failing to make a payment within 60 days of filing a CRN will also count as acting in bad faith.

If the insurance company fails to even respond to your claim within 60 days of filing the CRN, then your bad faith claim may mirror the outcome of Harper’s case against GEICO.

Is Your Florida Insurance Company Acting in Bad Faith?

Bad faith claims should be a last resort for Florida insurance policyholders. That said, if you genuinely believe that your insurance company is acting in bad faith, it’s time to take action.

When you sign a contract for coverage, you should not have to suffer because your insurance company is not holding up their end of the deal. Talk to a Florida personal injury lawyer about filing a bad faith claim against your insurance company.

About the Author:

Andrew Winston is a partner at the personal injury law firm of Winston Law. For over 20 years, he has successfully represented countless people in all kinds of personal injury cases, with a particular focus on child injury, legal malpractice, and premises liability. He has been recognized for excellence in the representation of injured clients by admission to the Million Dollar Advocates Forum, is AV Preeminent Rated by the Martindale-Hubbell Law Directory, enjoys a 10.0 rating by AVVO as a Top Personal Injury Attorney, has been selected as a Florida “SuperLawyer” from 2011-2017 – an honor reserved for the top 5% of lawyers in the state – and was voted to Florida Trend’s ”Legal Elite” and as one of the Top 100 Lawyers in Florida and one of the Top 100 Lawyers in the Miami area for 2015, 2016, and 2017.